Approved in under five minutes.

A customer-facing loan portal that decides on its own. From the moment the applicant taps submit, RiskScout takes the file through KYC, income parsing, scoring and the rule engine — and lands on a preapproval in under five minutes. Nobody on the bank side touches it.

Pre-approved amount

€ 25,000

Elapsed

4:12

Two years embedded inside a regional bank. RiskScout came out of it.

The applicant taps submit. Four minutes later they see their decision. The underwriting team only sees the file when the model can't handle it on its own — which, in the standard path, is almost never.

From tap to greenlight.

What actually happens during those 4 minutes and 12 seconds. No human in the loop unless the rule engine flags one.

Application starts

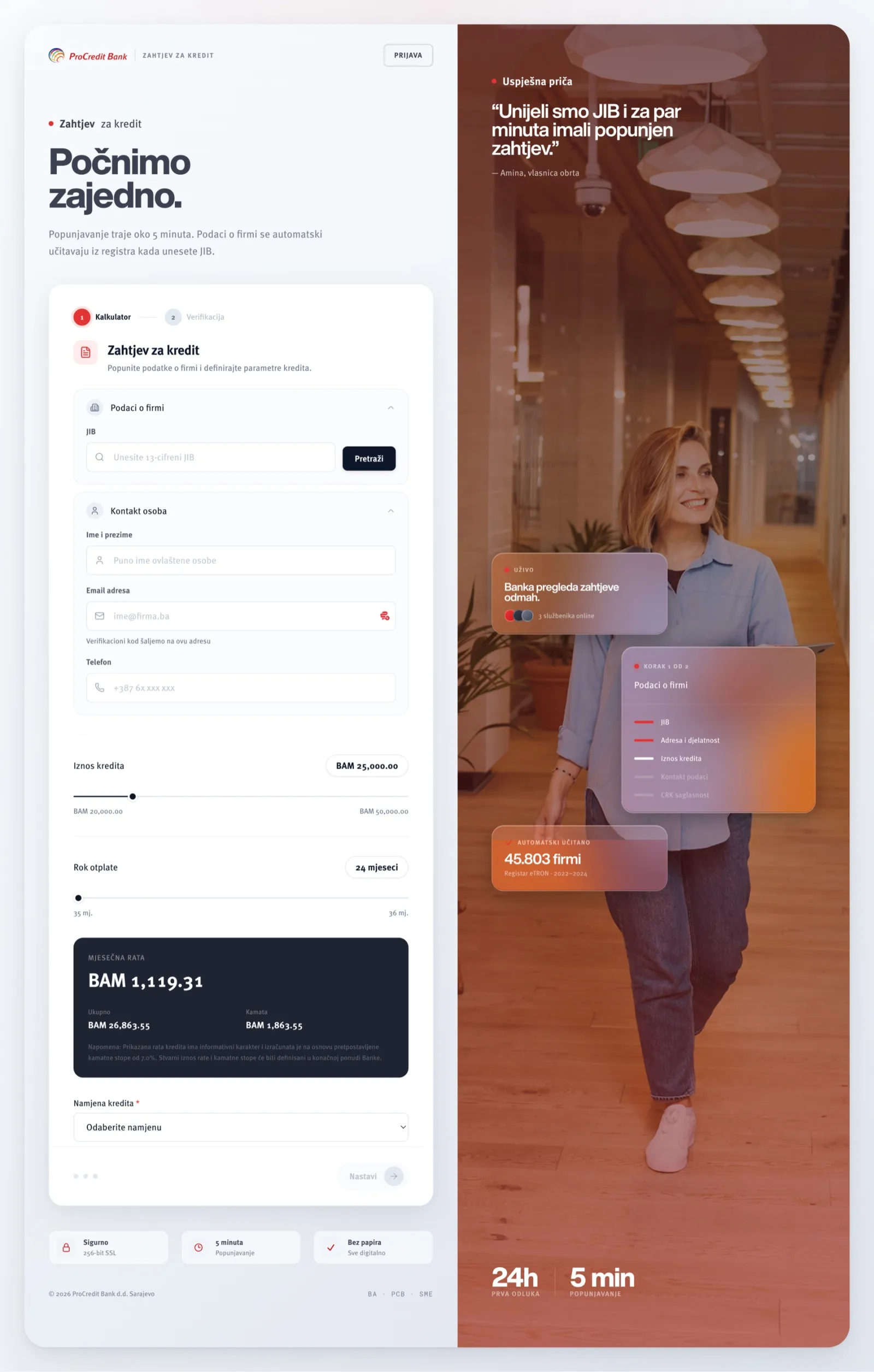

Customer lands on the portal — from a bank referral, a LeadHunter call, or a direct link. The form changes based on what they are asking for.

Identity verified

ID scan, selfie, liveness. Cross-checked against national registries and sanctions lists. No one at the bank looks at it.

Financials read

Bank statements and pay slips read line by line. Debt-service ratios checked against thresholds the bank set themselves.

Preapproval delivered

Risk model scores the file, the rule engine decides, the customer sees the result on screen. The underwriter gets a ping only if it's an edge case.

Six modules. One portal.

Pick the modules you need today, switch the rest on when your product lineup grows. The portal stays the same.

Application intake

Mobile-first form that changes based on what the customer is asking for. Document uploads, OCR, pre-fill from national registries where they exist.

Identity verification

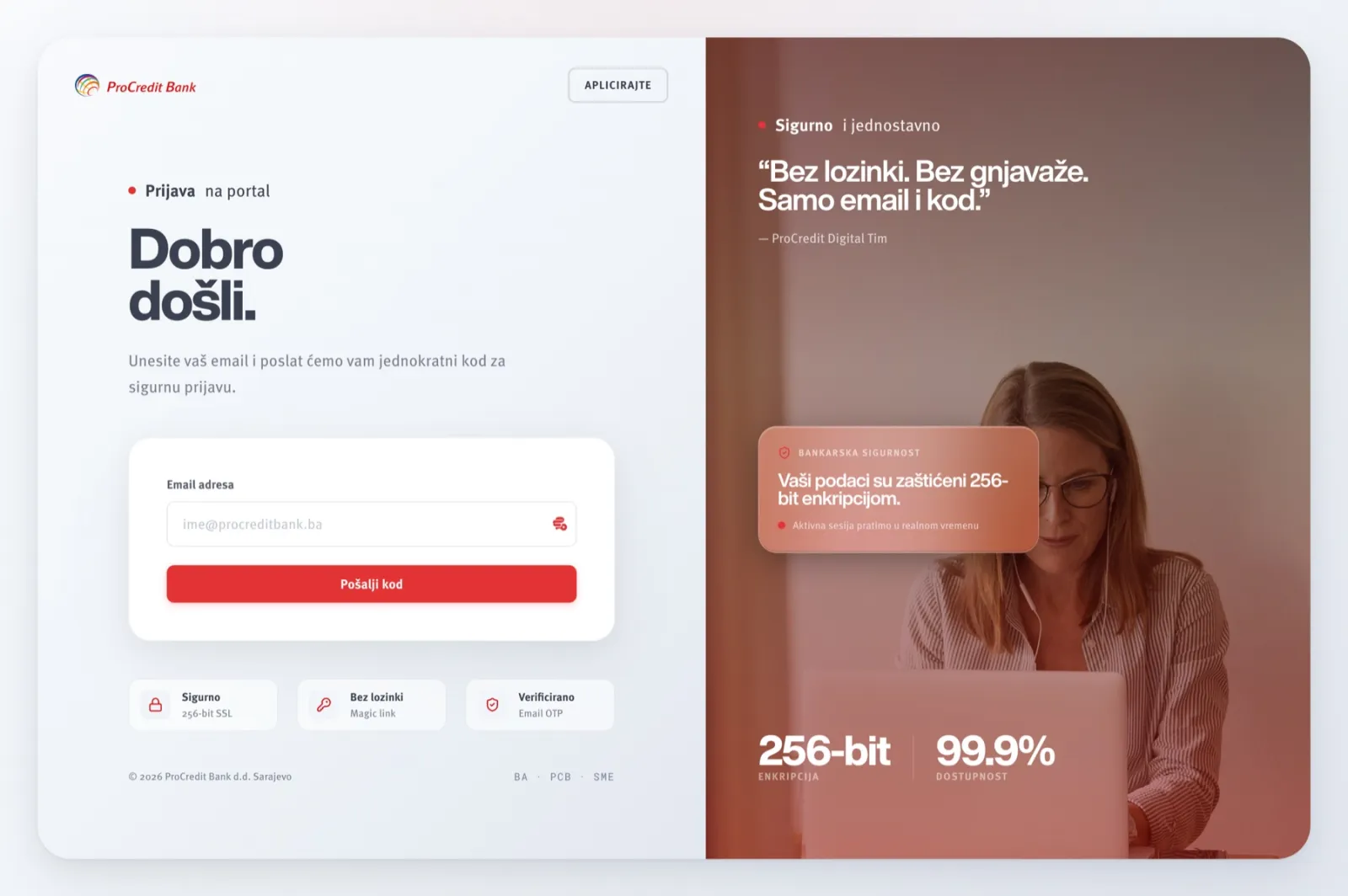

ID scan, selfie match, liveness, sanctions screening. Wired into national e-ID schemes where they exist, third-party providers where they don’t.

Income & affordability

Reads bank statements and pay slips line by line. Debt-service ratios checked against thresholds the bank sets — not us.

Risk scoring

A risk model you tune from a panel — per product, per region, per segment. Every score comes back with the reasons behind it.

Rule engine

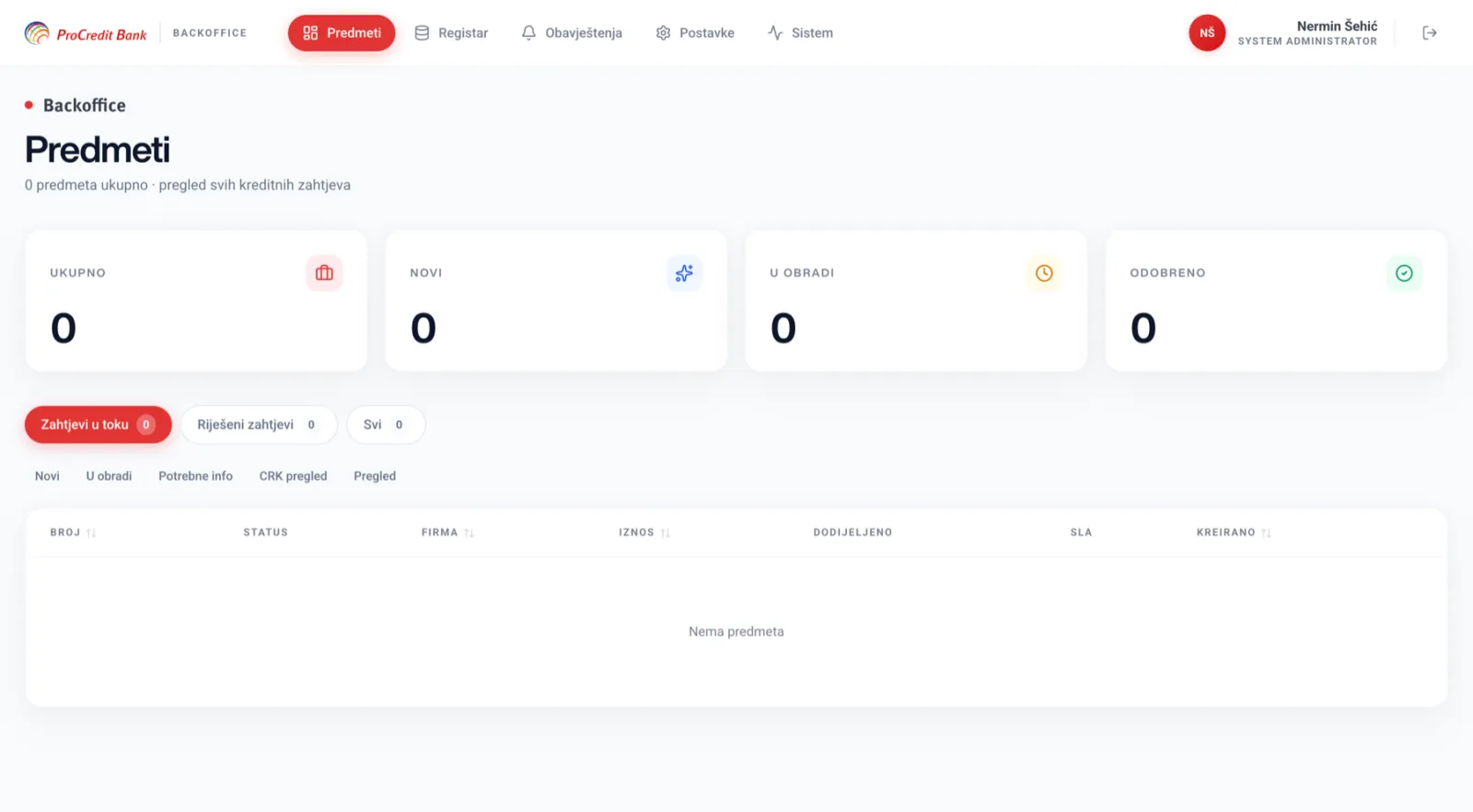

Sits on top of the model score. Auto-approve, auto-decline, send it to an underwriter — each path is a setting, not a code change.

Customer portal

Applicants track their file, upload what’s missing, get updates in one place. No email threads, no phone tag.

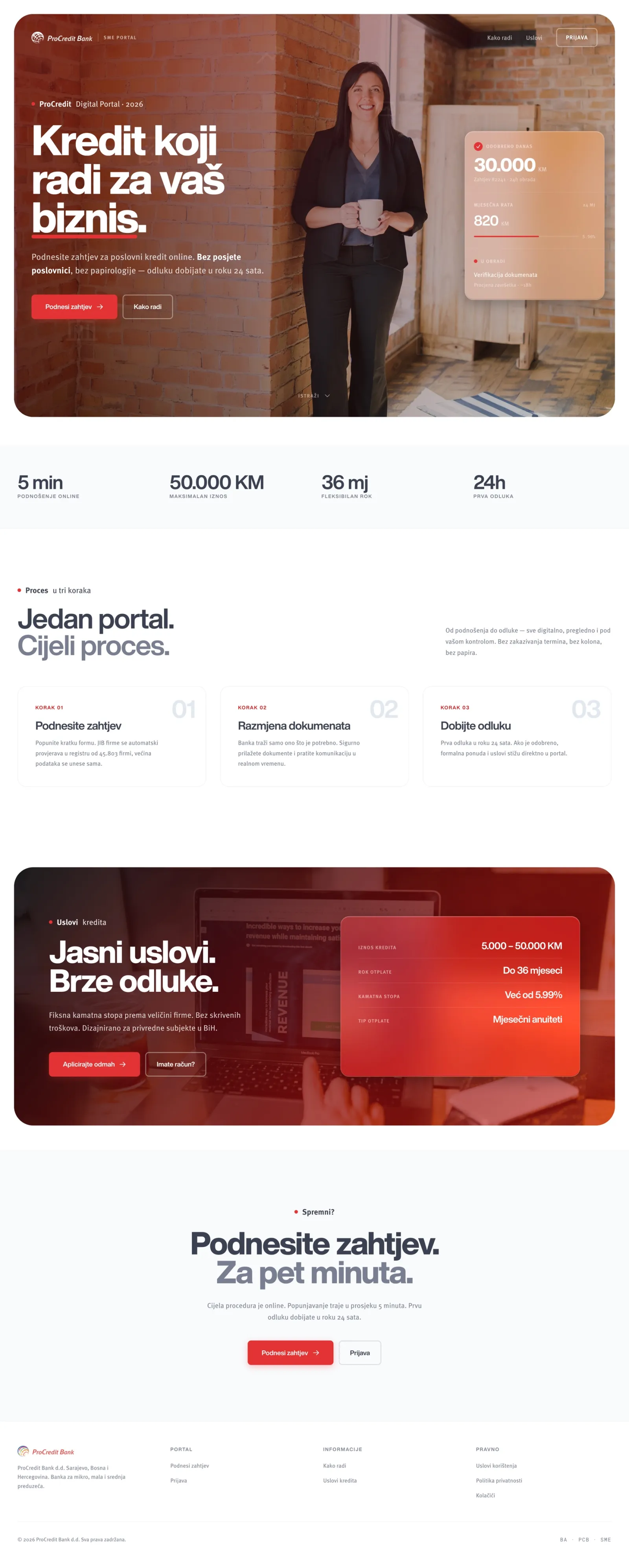

Live at ProCredit Bank.

RiskScout runs the SME lending portal at ProCredit Bank Bosnia today. Below: the actual product — customer landing, self-service application, the bank-side backoffice.

Built for regulators, not around them.

Every decision RiskScout makes is written down, versioned, and explainable. When a regulator knocks, you hand over the log. Not a phone tree.

Show us your riskiest workflow.

Half an hour, the actual product, running a real application end-to-end. Bring the case your current process keeps tripping over.